FinNexus Blog

FinNexus Blog

On the P&L of FPO Liquidity Pool

Ryan Tian — October 23rd 2020

Quantitive analysis of the behaviors of the liquidity pool under the MASP mechanism

In this article, we will take a closer look at the specific mechanisms of our Multi-Asset Single Pool (MASP) peer-to-pool DeFi options model with specific calculations. Hopefully, this article will give the users a clearer idea of how the multiple assets’ price movement and the BTC/ETH price movement may affect the liquidity pool’s financial behavior.

Previously, FinNexus introduced the MASP model, the pool with multiple assets, potential risks, and the security mechanisms in the building of the FinNexus Protocol for Options (FPO). Please have a look at these previous articles to get a comprehensive idea of the options platform available at options.finnexus.io.

The potential loss of the pool as the collective writer of options

Options are normally bilateral contracts that allow the option holders to buy or sell an underlying asset at a predetermined price within a set time frame. The options writers/sellers have fixed gains, while theoretically, the potential loss can be unlimited.

In FPO with the MASP mechanism, the option sellers are collected together into a single liquidity pool, jointly working as the counterparty for all options. The risk faced by a single option is diversified in the pool automatically.

For risk control reasons, it is still very important to analyze how the pool’s net value will behave in some extreme cases.

Suppose:

The current BTC price is 10,500 USD and the ETH price is 360 USD.

We have the liquidity pool with ETH, USDC, and FNX, and these three crypto-assets contribute evenly to one-third of the pool value respectively.

The value of the assets in the pool remains stable. (For simplicity of calculation, we ignore the price movement of the assets in the pool, even for ETH.)

Options are at-the-money (ATM).

The options written by the pool reach the maximum amount, which means that the collaterals get to the Minimum Collateral Utilization Ratio (MCUR) and the collateral in use is 100%.

FPO has options with two underlying assets, BTC and ETH, with a 1:1 ratio in the live options.

According to the Options trading experience in traditional finance, the probability of winning on the sellers’ side when writing ATM options is 80% on average.

Options are written with the expiration of 1d, 2d, 3d, 7d, 14d, and 30d; at the proportion of 10%, 15%, 20%, 30%, 15%, and 10%, based on the option volumn on centralized exchanges.

The price movement of BTC and ETH follows the habit of normal distribution. The probability of movement between -2σ and +2σ is 95.44%, therefore we assume that the price movement will be most likely in this range.

Assuming that the price moves in the unfavorable direction to the extreme of the maximum 2σ level, when the option writers suffer losses.

We took the BTC price data every day in the past 3.5 years from Cryptocompare, and made the following calculation:

BTC options in FPO

Calculation of potential loss of FPO based on BTC historical datadocs.google.com

The max loss ratio to the pool is -0.37%.

We took the ETH price data every day in the past 3.5 years from Cryptocompare, and made the following calculation:

ETH Options in FPO

Calculation of potential loss of FPO based on ETH historical datadocs.google.com

The max loss ratio to the pool is -0.36%.

Therefore, we have an average max loss ratio to the pool at about -0.37%. This is not bad at all considering an assumption of an extremely unfavorable market movement. It shows that with the security mechanisms provided in MASP, the risks from writing options are largely distributed and controlled.

Nevertheless, there is an assumption that the value of the assets in the pool remains stable. Let’s take another look at how the pool will behave if the price of the pool composition changes.

How the price change affects the multi-asset contributors in the pool

(On the official release on Ethereum since 4th Oct. 2020, FPO v1.0 changes to two pools with $FNX and $USDC as the single asset respectively. Therefore, this article may not apply to FPO on Ethereum. But it still applies to the model on Wanchain, with $WAN and $FNX as acceptable assets in the pool. But one may need to change $ETH or $USDC to $WAN in the following analysis)

As we put it here, participants may contribute ETH, USDC, or FNX to the liquidity pool, thus the pool works like a mutual fund, consisting of these 3 types of crypto-assets.

The pool net value is measured in USD. When a user entering into the pool, no matter what type of assets one contributes, the number of pool shares as in FPT (‘FinNexus Pool Token’) is calculated in the USD value at the time of entry.

For example, if one transfers $180 of ETH into the pool and the FPT at that time is 0.9 USD, then he/she may get 200 units of FPT tokens.

Since the pool behaves like a mutual fund with 3 types of assets, ETH, USDC, and FNX, the relative price changes of these assets may affect the net value of the pool. Suppose there are no gains or losses from the issued options, and let’s take a closer look.

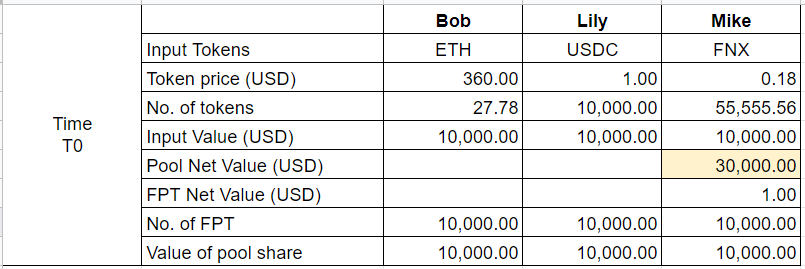

Here are some examples :

We have three contributors, Bob, Lily, and Mike, and each contributes $10,000 worth of ETH, USDC, and FNX in the pool respectively.

Examples of pool behaviors due to the price changes

How the price changes may affect the pool participants’ profit and lossdocs.google.com

As shown in the working sheet above:

(1) At time T0, each of the three joins the pool with an equal USD value of ETH, USDC, and FNX respectively. The total pool net value is $30,000. The pool has 30,000 shares in FPT and the FPT net value is $1.

(2) At time T1, suppose ETH price increases 30% and FNX drops 20%. The total pool net value increases to $31,000. With the total FPT stays unchanged, the FPT net value increases to $1.03 accordingly. If any of the three withdraws out of the pool, he/she may get $10,333.33 worth of tokens, but the composition of tokens may be different from the ones when he/she deposits.

Consequently, Bob gets 22.08 ETH; Lily gets 10,000 USDC and 0.71 ETH; Mike gets 55,555.56 FNX and 4.99 ETH. The details are shown in the form.

(3) The same logic applies in the scenarios of T2, T3, and T4 when the market price of ETH and FNX make different moves. The total pool net value and FPT net value change accordingly and the three participants will get a different basket of assets when withdrawing out of the liquidity pool.

Summary

MASP provides some interesting new mechanisms to the behaviors of the liquidity pool in FPO. It collectively works as the counterparty for all options, and also, it is working under the rules of a mutual fund, with the composition of the three assets. The proportions and relative price movement of these assets may have an influence on the financial behavior of the pool.

Now as the FPO WildNet comes to a closure, we will evaluate the questions and suggestions from our community, as well as all the many options we’ve been suggested for improvement, before introducing the official FPO to the general public.

Stay tuned!

About FinNexus

FinNexus is building a suite of open finance protocol clusters that will power hybrid marketplaces trading both decentralized and traditional financial products. The headline product released is a fully decentralized options model with pooled liquidity, live on both Ethereum and Wanchain.

***Newsletter | Whitepaper | Telegram | Twitter | Linkedin | Facebook| Discord***